If you frequently make online payments but remain concerned about your sensitive bank account details, these seven virtual credit card services can give you the added layer of protection you need.

What Are Virtual Credit Cards and How Do They Work?

A virtual card is a temporary card designed to protect the details of your real cards from falling into the wrong hands. When you use a virtual card to make an online payment, the money is deducted from your bank account and the credit account of your virtual card provider. Still, you won’t have to reveal the details of the physical credit card associated with it.

However, the transaction will be visible in your bank account statement as though you used a regular credit card. Yet, you will not run the risk of compromising your personally identifiable information. For example, the card number being used is from your temporary card instead of your physical one.

In other words, if a hacker gains access to your virtual card information, it will be of no use to them, as you can easily cancel the card without having to change your entire account. And if you are using a single-use virtual card, it will automatically expire after a transaction, so it will no longer be useful to any fraudster online.

This system of redirecting payments through a virtual card makes it very safe to send or spend money online and protects you from credit card fraud.

Also read: Top 5 Android Wallets to Store Gift Cards, Tickets, and More

What Are the Drawbacks of Virtual Credit Cards?

Even though you get an additional layer of security with virtual cards, there are some situations where having a virtual card could backfire. Virtual card numbers are temporary and different from your actual credit card, which can sometimes create confusion between you and the merchant.

For example, if you want to return something that you bought on Amazon, your refund will be initiated in the account you used to pay for it in the first place. But if you use a disposable virtual card that you destroyed after your purchase, you won’t be able to avail your refund and may have to settle for store credit instead.

Similarly, if you use a virtual card to rent a car or make a reservation for a hotel, you may be required to share your account number with them. However, since virtual card numbers are not real account numbers, you could face issues verifying your details with them.

However, these issues are still minor compared to the benefits and security that virtual cards offer. And now that we know what virtual cards are and how they work, let’s move on to the actual list. Here are the seven of the best virtual credit card services.

Also read: Venmo vs. Zelle: The Best Digital Wallet to Send Money Easily

1. US Unlocked

US Unlocked offers virtual Visa debit cards and prepaid cards accepted by most U.S. retailers. In addition, these cards come with a billing and shipping address in the United States, which makes transactions with U.S. retailers more convenient.

Two types of cards are offered. One is a single-use card that you can use to make a single transaction. After which, it will be disposed. But if you want to make regular payments to a single vendor, you can use the merchant-specific card that locks on a specific merchant like Walmart or Netflix after a successful payment.

Once you create a virtual credit card, you just have to pay a small one-time fee and top it up with as little as $50 before starting to use it. Also, if you subscribe to any streaming service, like Netflix, Hulu, HBO Max, etc., with the U.S.-unlocked card, you can access the U.S. version of these websites because of the local shipping address.

The account top-up fee varies from 3% to 7%, depending on the payment method you use and the amount of money you put in the card. They also have fixed charges like $0.50/transaction and $3.50 to $4 on every account top-up.

Pros:

- Easy check out extension

- Access U.S. version of streaming websites

Cons:

- Slightly expensive

Also read: How to Use Google Pay to Track Your Spending and Budget Your Money

2. Wise

Wise has recently started a virtual credit card service that has a lower fee structure and offers a ton of features – just like its payment protocols.

With Wise, you can have up to three virtual credit cards at a time. In addition, you can set custom limits to your cards and lock them with a specific merchant. You can also shop anywhere in the world using Wise’s virtual credit cards, and the money will be deducted directly from your digital wallet, like Google Pay or Apple Pay.

It means you can carry out the smallest transactions without revealing your real UPI address, and the best part is that you even get real exchange rates on all your international transactions.

Even though you can minimize the risk by setting up custom limits, if you still feel like your data is being compromised, you can immediately freeze your virtual card so that it’s impossible to access by an outsider.

You can immediately unfreeze it just as easily in the future if you think it’s safe to use. This feature gives you the manual security of your virtual credit card in your hand, as it only activates once you use it.

Wise virtual credit cards support more than 50 different currencies, and the services are available in more than 30 countries. Moreover, the virtual credit card is free for all Wise account holders except customers from the U.S. and Japan.

Pros:

- Freeze and unfreeze cards with ease

- Supports more than 50 currencies

- Service available in more than 30 countries

Cons:

- Service is not free for the U.S. and Japan-based account holders

Also read: How to Make Venmo Private And Protect Your Privacy

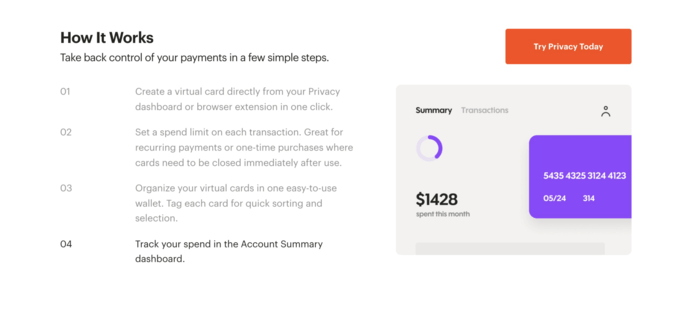

3. Privacy

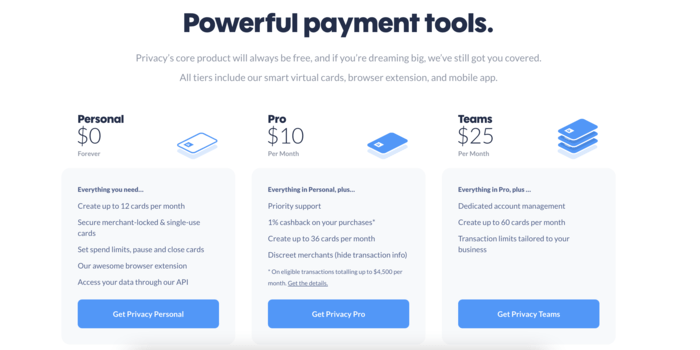

Privacy virtual cards are perhaps the easiest to sign up for, and you can get a virtual card for free. However, they do have premium plans that go from $10 to $25, depending on your use case and transaction limits.

With their free plan, you can create up to 12 virtual cards and customize them to best fit your spending. In addition, you can set merchant locks and expenditure limits on each card and create single-use cards that expire after each transaction.

But Privacy cards are not really credit cards; you can think of them more like single use virtual payment cards, as all the transactions you make through the cards are deducted from your bank account directly. It means you don’t get an extended period or any outstanding balance buffer, as all the transactions are fulfilled in real time.

However, it stills adds a ton of safety features and serves the purpose of cloaking your original account details while making online transactions. Privacy also offers a browser extension to quickly checkout while shopping online using the virtual cards.

You can also freeze and unfreeze your cards with the click of a button. It makes shopping online and subscribing to services with auto-renewal even safer.

The best part about Privacy cards is that they don’t charge their customers anything for any online transaction. If you are fine with using 12 cards a month, you can easily get away with their free plan. Privacy is able to provide the plan for free, as its main source of revenue is the money it makes off interchanges at the merchant’s end.

Pros:

- Very easy to set up

- One-click checkout with a browser extension

- Free plan limits are enough for most users

Cons:

- No credit functionality

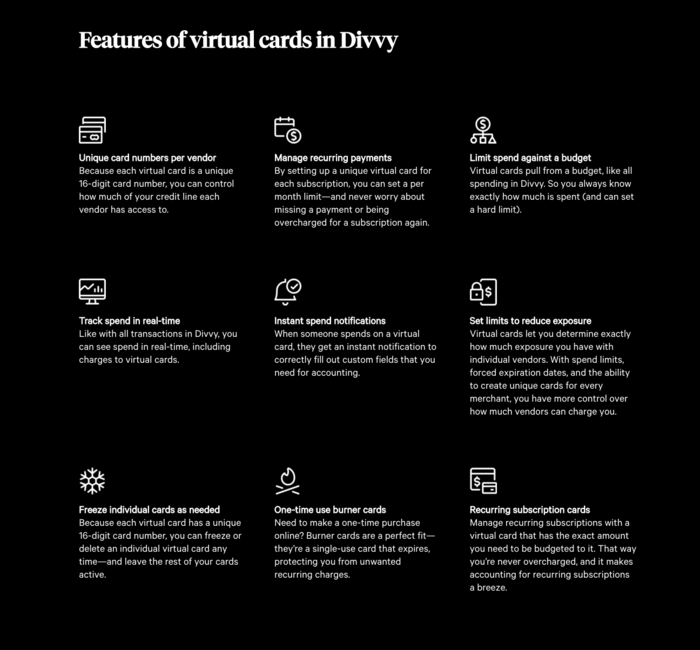

4. Divvy

Divvy is more than just a virtual credit card provider. It’s a financial service provider that helps businesses by providing credit lines of up to $15 million and offering excellent tools to manage their expenses.

Using this platform, you can easily create preloaded cards for multiple use cases like marketing, business trips, and miscellaneous company expenses and allocate a custom spending limit for each of them.

You can also monitor and control all of your company’s expenses through a single dashboard. In terms of control features, Divvy virtual cards allow you to set a spending limit and manage all your card activity through Divvy’s budgeting software.

With Divvy, you can issue one-time burner cards that are good for a single use. You can set them up with a budget limit or an expiration date or opt for multi-use recurring subscription cards that can be set up with monthly funds. You can also add custom limits.

What makes Divvy one of the best virtual credit card services is that it’s completely free to use, and you can use both Divvy’s cards and software without paying a membership fee or fixed charges. Additionally, a reward scheme is also provided along with multiple benefit packages.

Pros:

- Free-to-use service

- Reward schemes and benefit packages

Cons:

- Poor customer service

Also read: Apple Pay Not Working? Here’s How to Fix it

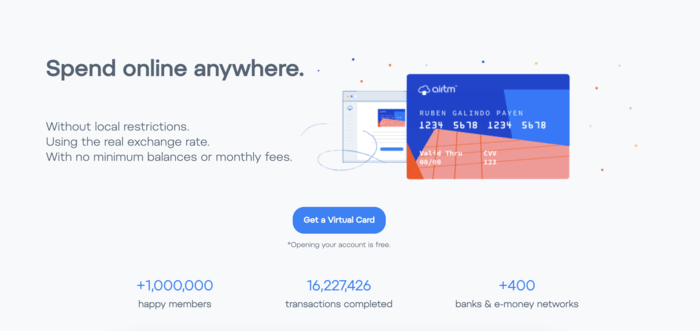

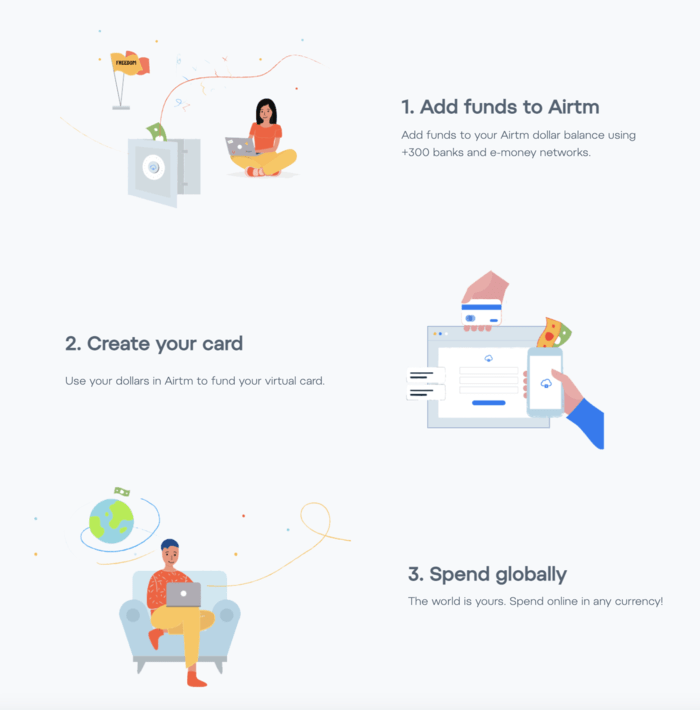

5. Airtm

Airtm is a digital banking service that allows users to store, send and even make direct payments. It has recently started offering virtual cards to users that come with a ton of features and benefits.

Airtm card’s custom limits depend on customer verification. As a verified user, you can create up to five prepaid virtual cards with a minimum balance of as low as a dollar, and you also get a monthly card limit of up to $2400. However, things get a little restrictive if you are not a verified user. You can make up to ten virtual cards but only get a spending limit of $1000 a month.

Irrespective of whether you are a verified user or not, you can still create both single-use cards that are good for one online transaction or a reusable card with no expiry date.

The Airtm virtual card service is unique because it allows you to trade and recharge your virtual card using cryptocurrency. It is made possible by Airtm’s excellent peer-to-peer service that allows your Airtm funds to be connected to more payment methods. However, Airtm is not the most generous when it comes to charging for its services.

Depending on your verification status, creating any virtual payment card and loading it up will cost you anywhere from $3.70 or $4.95. You will also be charged a 3% top-up fee along with a 1% service fee. And even though they offer unlimited transactions, they charge an additional fixed fee of $1 per transaction.

Pros:

- Directly buy virtual currencies using a virtual card

- Add money to your virtual prepaid card from more than 800 banks

Cons:

- Expensive

Also read: How to Remotely Disable Apple Pay

6. Stripe

Stripe is an outstanding money transfer service that offers virtual credit cards that are easy to set up and have an equally easy signup. You can issue a virtual card from their website without engaging in any long-term contracts or paying setup fees.

What sets Stripe apart is that they allow you to create as many cards as you want without paying any monthly charges. Additionally, their cards offer a wide range of customization through their programmable card controls. You can configure your cards, designate particular merchants and issue one-time or multiple-use cards in just a few clicks.

Stripe has a very interactive dashboard that presents your account statistics in a very easy-to-read format. Using this dashboard, you can also update your spending controls, create more cards and freeze or unfreeze existing cards.

Stripe allows you to create advanced combinations of rules using their API management services so that you have full control over your virtual payment card.

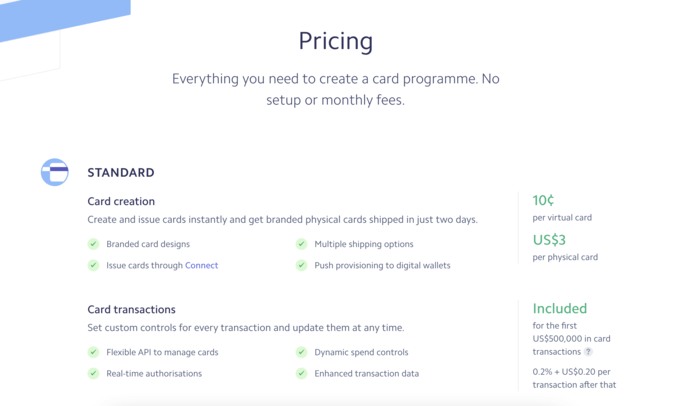

As for the payment scheme, Stripe charges justifiable rates for its services. It charges 10¢ per virtual payment card and has a maximum spending limit of over a million dollars in a single transaction.

However, you are not charged anything for transactions of up to $500,000, after which you will have to pay 0.2% + $0.20 per transaction after that. Also, if you want to make cross-border transactions, Stripe requires you to pay an additional 1% fee for currency conversion.

Pros:

- Easy to set up

- No transaction fee up to $500,000

- Detailed account controls and real-time insights

Cons:

- UI isn’t the most intuitive

7. Emburse

Emburse offers digital credit and debit cards for businesses to help pay employees and contractors safely and seamlessly.

it also have its own ecosystem that allows businesses to automate their purchase and expense categorization and track down their transactions remotely from anywhere in the world. Businesses can also view their expenditure reports and insights in real time and instantaneously manage their funding requests and approval.

And just like most reputed virtual payment card providers, Emburse also allows you to manage your spending limits and tie a single card to a merchant. All of this is supported by its world-class fraud protection algorithm that prevents business accounts from theft or from being compromised due to any data leak or hacking.

The best part is that Emburse offer its services free to businesses with 100 employees. It also offers custom plans for large-scale businesses, but rates vary depending on the company size.

Pros:

- Apple Pay integration

- Automatically create reports and stats

Cons:

- Not for personal use

Frequently Asked Questions

1. Can I add virtual payment cards to Apple Wallet or Google Pay?

Both Google Pay and Apple Wallet come with the option to link your virtual card. All you have to do is enter the details of your virtual payment card and follow the on-screen instructions to successfully add it to your wallet. After this, your virtual payment card can pull funds directly from your Apple Wallet or Google Pay.

2. What is the difference between virtual credit cards and virtual payment cards?

A virtual payment card is simply a proxy of your debit card, as you can add money to it and spend it anonymously online. Virtual credit cards allow you to take a small loan that you have to pay back at the end of the month.

3. Can a virtual card affect a credit score?

Virtual credit cards may or may not affect your credit scores. When you create a virtual account from any financial institution, it’s their choice to send your records to the credit bureau. So if you have signed up for a virtual credit card directly from your bank, your credit scores will be calculated based on your payment timing. However, most third-party virtual card providers don’t share your credit scores with the bureau.

4. Are free virtual cards safe to use, and how do free virtual card companies make money?

Most free virtual credit card services such as Privacy and Divvy are safe to use and generate revenue by earning commission from the interchange between you and the merchant. For example, if you purchase something from Amazon using one of their free virtual cards, they will charge Amazon instead of you for accepting the payment through the virtual card.